All Resources

Unlocking Your Home’s Potential: The Comprehensive Guide to HELOCs vs. HELOANs

Learn the difference between a Home Equity Line of Credit and a Home Equity Loan and how to protect your low mortgage rate.

Key Takeaways:

- Protect Your Low Mortgage Rate: Don't sacrifice your current low mortgage rate just to get extra cash. By choosing a HELOC or HELOAN, you can tap into your home's equity through a second mortgage, preserving the competitive terms on your primary loan.

- HELOCs = Flexibility: A Home Equity Line of Credit is a revolving credit line. It’s ideal for multi-phase home renovations or acting as an emergency fund, letting you draw funds only as needed (often with interest-only payment options).

- HELOANs = Predictability: A Home Equity Loan provides a lump sum upfront with a fixed interest rate. It's the best tool for consolidating high-interest debt or paying for one-time major life events (like a wedding or tuition) with a predictable monthly payment.

For many homeowners, your residence is your largest single investment. Over the past few years, as property values have continued to increase, a significant amount of wealth has been built that often sits "trapped" in your walls.

The challenge isn’t just knowing that you have equity; it’s knowing how to deploy it strategically. Through BankUnited’s partnership with Spring EQ, we are able to bridge the gap between traditional banking security and modern fintech speed. Whether you are looking to increase your home’s resale value, consolidate high-interest debt, or fund a major life milestone, understanding the nuance between a Home Equity Line of Credit (HELOC) and a Home Equity Loan (HELOAN) is the first step toward a smarter financial future.

To help you navigate these options, we’ve created this comprehensive guide to break down the strategic advantages, and the key differentiators that make BankUnited’s Home Equity Loan Options Powered by Spring EQ the right choice for your next chapter.

The No-Refinance Mortgage Protection Strategy

In 2026, the most valuable asset a homeowner can possess is a low-interest primary mortgage. If you secured a rate between 3% and 4% a few years ago, that rate represents thousands of dollars in annual savings.

The biggest mistake a homeowner can make today is a "Cash-Out Refinance." Refinancing your entire mortgage just to access $50,000 in equity means you are essentially "trading in" your low interest rate on your entire home balance for a higher market rate.

The BankUnited Advantage

Our home equity solutions are structured as subordinate financing. This means you keep your first mortgage exactly where it is. You preserve your low rate and simply add a second layer of financing. This approach gives you access to your liquidity to get the cash you need, without sabotaging the wealth you’ve already built.

Flexible Funding: HELOC Optimizes Your Cash Flow

A Home Equity Line of Credit (HELOC) is a revolving line of credit that allows you to borrow, repay, and borrow again during a set "draw period."

How Your HELOC Limit is Determined

At BankUnited, your borrowing power is determined by a calculation known as the Combined Loan-to-Value (CLTV) ratio. While many national lenders conservatively cap this at 80%, our partnership with Spring EQ allows for a 90% CLTV threshold on qualified primary residences.

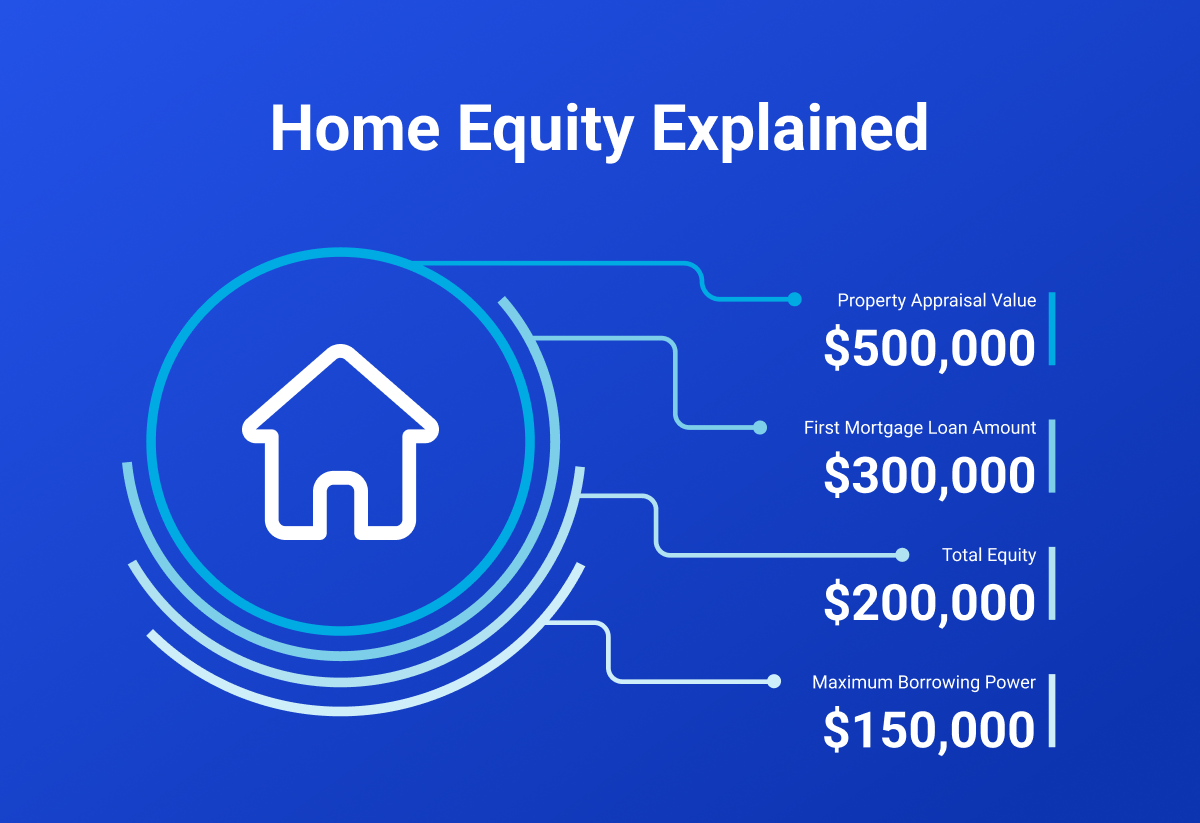

The Mathematics of Your Equity:

- The Valuation: We establish the current market value of your home through a streamlined appraisal process.

- The 90% Benchmark: We calculate 90% of that appraised value.

- The Existing Debt Deduction: We subtract the remaining balance of your current first mortgage from that benchmark.

- The Result: The remaining figure represents your maximum line of credit.

Example: If your home appraises for $600,000, the 90% benchmark is $540,000. If your current mortgage balance is $400,000, you could be eligible for a HELOC limit of up to $140,000.

Common scenarios when a HELOC meets your needs:

- The "Phased" Renovation: If you are doing a "slow flip" of your own home—starting with the bathrooms this year and the kitchen next year—a HELOC allows you to pay for each phase as it happens.

- The Ultimate Safety Net: Many homeowners open a HELOC even if they don't have an immediate project. Because it costs nothing to keep the line open, it acts as a massive emergency fund that is significantly cheaper than any personal loan or credit card.

- Interest-Only Flexibility: Through BankUnited’s Home Equity Line or Loan Powered by Spring EQ, we offer interest-only payment options for up to 10 years. This allows you to maintain maximum cash flow during the construction phase of a project.

Predictable Performance: The Fixed Rate HELOAN

A Home Equity Loan (HELOAN) is a traditional "closed end" loan where you receive a lump sum of cash on day one.

How Your HELOAN Amount is Determined

Like the HELOC, the HELOAN amount is rooted in the 90% CLTV calculation. However, because this product involves a lump-sum payout and a fixed repayment schedule, we also evaluate your Debt-to-Income (DTI) ratio.

This ensures that the new, fixed monthly payment aligns with your long-term financial health. By offering a 90% LTV ceiling, BankUnited provides access to a larger portion of your home's value than the industry standard, which is particularly beneficial for those looking to maximize their liquidity.

Common scenarios when a HELOAN meets your needs:

- High-Interest Debt Consolidation: This is the primary driver for HELOANs. By swapping 22% credit card debt for a single, lower-rate fixed payment, homeowners save an average of $530 per month according to the Spring EQ.

- One-Time Life Events: Funding a four-year tuition bill, paying for a wedding, or covering a major medical expense is a perfect fit for a HELOAN because the costs are known upfront.

- Fixed-Rate Security: Because the rate is fixed, your monthly budget is immune to market fluctuations. You know exactly when the loan will be paid off.

Why BankUnited Home Equity Powered by Spring EQ is Different

When searching for home equity options, our partnership with Spring EQ is the superior choice for modern homeowners:

- The 11-Day "Fast-Track" Funding: Traditional bank HELOCs can take 45 to 60 days to close. Our digital-first process aims to move from application to funding in as few as 11 days. We’ve removed the paperwork mountain in favor of a streamlined, secure digital experience.

- High Loan-to-Value (LTV) Accessibility: Most national lenders cap your borrowing at 80% of your home’s value. We offer up to 90% LTV for qualified primary residences. That extra 10% can be the difference between a minor update and a total home transformation.

- Inclusive Credit Requirements (640 FICO Floor): Many lenders require a 720+ credit score for equity products, but we believe home equity should be a tool for financial improvement. With options for FICO scores as low as 640, we help more homeowners utilize their assets to improve their overall financial health.

- Expert Guidance at Every Step: Every BankUnited Home Equity Powered by Spring EQ applicant is paired with a dedicated loan expert. You get the speed of a fintech app with the personal guidance of a professional banker who understands your specific goals.

The Financial Impact: Tax Benefits & ROI

While we recommend consulting a tax advisor, one of the most enduring benefits of a HELOC or HELOAN is the potential for tax-deductible interest. If the funds are used to "buy, build, or substantially improve" your home, you may be able to deduct the interest paid.

Beyond taxes, consider the Return on Investment (ROI). Using equity to replace an aging roof or upgrade a kitchen doesn't just improve your quality of life, it protects and increases the resale value of your most important asset.

Which Path is Yours?

Choosing between a HELOC and a HELOAN isn't about which product is "better"—it’s about which product matches your life's current phase in conjunction with your financial goals.

- Choose the HELOC if you prioritize flexibility. It is the ideal choice for those who want a revolving safety net, lower initial interest-only payments, and the ability to fund multi-phase projects as they arise.

- Choose the HELOAN if you prioritize certainty. It is the premier tool for those who want a fixed rate, a predictable monthly budget, and a clear, structured path to becoming debt-free.

Regardless of the path you choose, the BankUnited and Spring EQ partnership ensures you can access your equity without touching your low-rate first mortgage. We provide the capital and the insight to ensure your home remains a high-performing asset in your portfolio.

Ready to Unlock Your Equity?

The process takes less than 3 minutes to start. Check your personalized rate, verify your eligibility, and find out how much equity in your home you can put to work today.

This material is for informational purposes only and does not constitute an offer to extend credit or a commitment to lend. All lines of credit and loans are subject to credit approval, underwriting requirements, and eligibility criteria. Additional restrictions and limitations may apply.

SUGGESTED ARTICLES

All content is for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult your legal and tax or accounting advisors before making any financial decisions.