Compare Small Business Checking Accounts

PRIMARY BUSINESS CHECKING

minimum opening deposit

- $12 monthly maintenance fee - Avoid maintenance fee by maintaining average monthly balance of $1500 or more

- Up to 150 free transactions (deposits, deposited items, checks & debits) per statement cycle

- Business VISA® Debit Card

- Bank on the go with online & mobile banking

BUSINESS EXPRESS CHECKING

minimum opening deposit

- $20 monthly maintenance fee - Avoid monthly maintenance fee by maintaining average monthly balance of $5000 or more

- Up to 300 free transactions (deposits, deposited items, checks & debits) per statement cycle

- Business VISA® Debit Card

- Bank on the go with online & mobile banking

COMMERCIAL ANALYSIS CHECKING

minimum opening deposit

- $20 monthly maintenance fee

- Earnings credit available to help offset monthly maintenance fees and other service charges

- Detailed analysis statements to help keep track of your business banking (upon request)

- Business VISA® Debit Card

- Online treasury management services to manage your company's payments, collections, reporting and account balancing

Business Checking Account Benefits

Regardless of your choice, each of our small business bank accounts is built to deliver value, convenience, and control for your business finances.

Online Bill Pay

Debit Card

eStatements

Online and Mobile Banking

Small Business Checking Accounts FAQs

The best business checking account depends on your transaction volume, balance, and banking needs. BankUnited offers multiple small business checking accounts to match different business sizes and activity levels.

You can open a business checking account by contacting BankUnited or visiting a branch. You will typically need business formation documents, identification, and an opening deposit.

Fees may include monthly maintenance charges, transaction fees, and cash processing fees. Many fees can be avoided by maintaining required balances.

Yes, BankUnited provides online and mobile banking tools so you can manage your small business bank account anytime, including payments, transfers, and account monitoring.

Additional Business Banking Solutions

Interested in a Business Checking Account?

Featured Insights

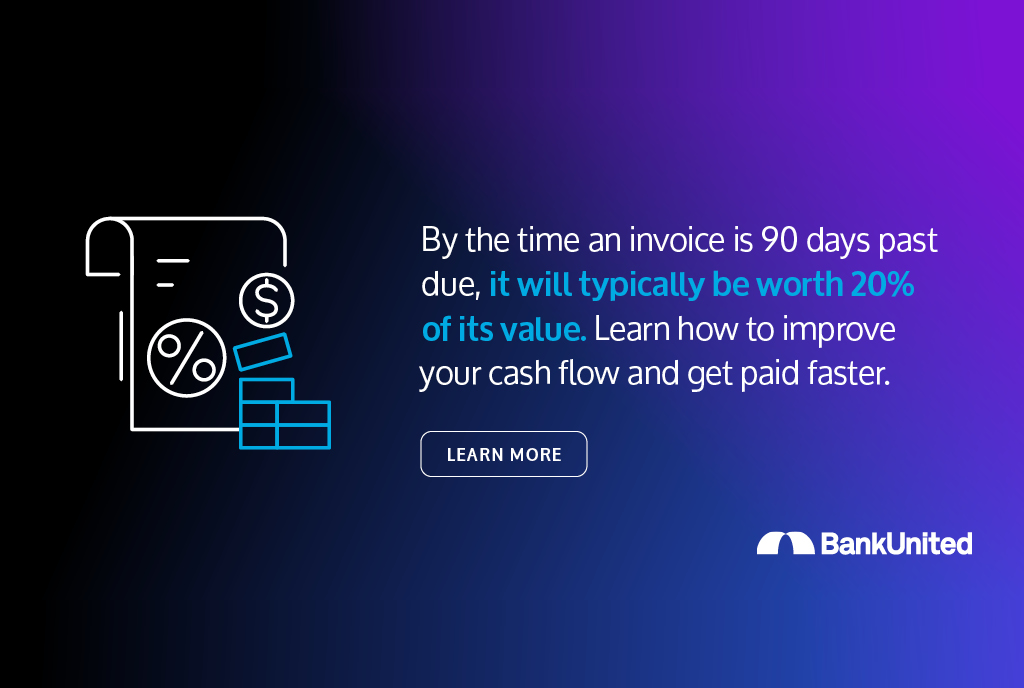

The Business Owner's Guide to Cash Flow

- What are my plans if cash flow is negative?

- How can I lower DSO? Is it possible to increase DPO?

- Does my business have more access to funding if needed?

- Are my cash flow numbers accurate?

- Is my business earning more than it is spending?

- How can my business increase profit margins?

- Small Business

- Article

Primary Business Checking Account

- $100 minimum opening deposit

- $12 monthly maintenance fee:

- Maintain $1,500 average monthly balance in the account or

- Maintain $4,500 minimum daily balance in related business checking or savings account1

- First 150 transactions per month at no charge

- Over 150: $0.40 transaction fee

- Cash Processing Limits: Deposit/withdraw up to $10,000 in cash per month at no charge

- $1.50 fee per $1,000 over $10,000

- Complimentary Business Visa Debit Card4

- Complimentary Online & Mobile Banking5

Automatically waived for the first two statement cycles (new accounts only).

Ways to avoid monthly maintenance fee:

Business Express Checking Account

- $100 minimum opening deposit

- $20 monthly maintenance fee:

- Maintain $5,000 average monthly balance in the account or

- Maintain $10,000 minimum daily balance in related business checking or savings account1

- First 300 transactions per statement cycle at no charge

- Over 300: $0.40 transaction fee

- Cash Processing Limits: Deposit/withdraw up to $15,000 in cash per month at no charge

- $1.50 fee per $1,000 over $15,000

- Complimentary Business Visa Debit Card4

- Complimentary Online & Mobile Banking5

Automatically waived for the first two statement cycles (new accounts only).

Ways to avoid monthly maintenance fee:

Commercial Analysis Checking Account

- $100 minimum opening deposit

- $20 monthly maintenance fee:

- Transaction fee applies3

- Cash Processing Limits: Refer to applicable fee schedule

- Complimentary Business Visa Debit Card4

- Online & Mobile Banking: Fees apply to Online Treasury Management Access6

Earns Credit available to offset fees2

- Related account must be in the same name as your Primary Business or Business Express Checking Account.

- The monthly maintenance fee may be offset by the earnings credit calculations applied on an analyzed statement at end of month. The earnings credit shall be equal to (i) the average monthly collected balance multiplied by (ii) the then applicable earnings credit rate divided by the actual number of days in the applicable year multiplied by (iii) the actual number of days in the applicable cycle. The earnings credit will be used to offset maintenance fees, transaction fees and any other service charges that may be assessed to the account. If the earnings credit rate exceeds the total monthly fees, such excess will not be carried over or applied to fees incurred in subsequent months. If the earnings credit is less than the total monthly fees, the account may be charged for the amount of the difference. If the earnings credit is negative, the account may be charged the full amount of the fees.

- Transaction fees are attained for the following and will be priced accordingly at the time you elect the service.

- For each check and/or debit paid per statement cycle

- For each ACH Credit per statement cycle

- Per deposit credited per statement cycle

- Per item deposited per statement cycle

- You'll get a BankUnited Visa® Business Debit Card with no-fee transactions at BankUnited ATMs. A $2.50 fee will be charged for each transaction performed at a non-proprietary ATM that is not within the Allpoint Network. Fees charged by the ATM owner/operator may also apply.

- Requires enrollment.

- Pricing provided by our Treasury Management team. Pricing may be different at the time you elect the service. Please contact a Treasury Management Officer for additional information.

Rates and annual percentage yields (APYs) are effective as of the date indicated and are subject to change without notice unless otherwise stated. Fees may reduce earnings on the account. Products, services, fees, terms and conditions are subject to change. Certain restrictions and limitations may apply. Contact BankUnited for complete account details.

Please review the see our Deposit Account Agreement, Business Schedule of Fees and Funds Availability Disclosure for complete details.